Reto Arnold

Ernst Giger

Case studies on the restructuring of partnerships

Case studies and detailed solutions by Reto Arnold and Ernst Giger from the ISIS seminar "Corporate Restructuring" on May 9, 2019.

Case study 1: Conversion of a partnership into a corporation

1.1 Basic facts

1.1.1 Initial situation

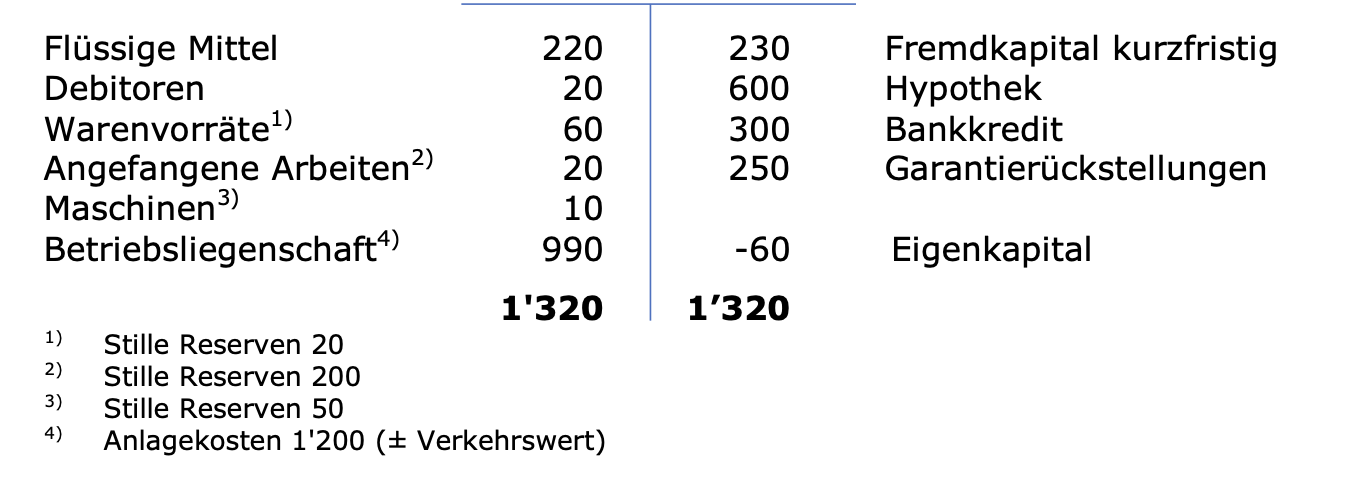

Johannes Immergrün has been running a metalworking business in the legal form of a sole proprietorship for many years. As at December 31, 2018, the provisional balance sheet of the sole proprietorship was as follows (in CHF thousand)

Immergrün is 63 years old and in poor health, which is why he wishes to gradually withdraw from active responsibility for the business. On the advice of his trustee, he intends to convert the sole proprietorship into a public limited company (Immergrün AG) with a view to succession planning.

1.1.2 Questions

- Can the sole proprietorship be converted into a stock corporation on the basis of the provisional balance sheet as at December 31, 2018?

- How do you assess the trustee's recommendation to build up the equity required for the conversion by revaluing the work in progress by CHF 160,000? Is his advice correct that the revaluation represents a liquidation gain subject to privileged taxation under Art. 37b DBG?

- Does the conversion of a sole proprietorship into a stock corporation lead to (further) tax and duty consequences?

1.2 Supplementary facts 1

1.2.1 Initial situation

As Johannes Immergrün has no suitable successor in the family or in the company, a succession plan with another company in the same sector is emerging. Knupp AG is prepared to take over Immergrün AG.

Based on the discussions to date, the two parties agree that

- Immergrün AG currently has an enterprise value of CHF 2,500,000,

- a legally binding solution for the takeover of Immergrün AG by Knupp AG should be reached today if possible.

In order to achieve the latter objective, the parties envisage that Knupp AG will acquire a 50% stake in Immergrün AG as part of the conversion of the sole proprietorship or shortly thereafter. The balance sheet would then be as follows (in TCHF):

.png)

In the shareholders' agreement, Johannes Immergrün and Knupp AG declare, among other things, their intention to carry out a capital reduction after 5 years, on the occasion of which Johannes Immergrün will return his shares for amortization, i.e. for sale, against payment of a (partial) liquidation dividend of CHF

2,500,000 (comprising the pro rata share capital of CHF 100,000 and the KER of CHF 2,400,000). The ABV provides for an adjustment of this liquidation dividend if a reduction in value occurs in the meantime that is directly attributable to Johannes Immergrün or for which he is responsible.

1.2.2 Questions

- Does the planned participation of Knupp AG in Immergrün AG as part of a capital increase (with a premium) violate the 5-year lock-up period pursuant to Art. 19 para. 2 DBG?

- What are the tax consequences of the capital reduction?

- Are there any other tax aspects to consider?

1.3 Supplementary facts 2

1.3.1 Initial situation

Following the capital increase carried out in accordance with Addendum 1, Johannes Immergrün and Knupp AG each hold a 50% stake in Immergrün AG. Johannes Immergrün fears that Knupp AG could ultimately decide not to acquire the remaining 50% of the shares in Immergrün AG after the expiry of the five-year lock-up period or not to agree to a subsequent capital reduction.

Johannes Immergrün's tax advisor is looking for a solution to ensure that the transfer of the remaining 50% of the shares in Immergrün AG and the planned capital reduction after expiry of the lock-up period are also

will effectively take place. To this end, it proposes that Knupp AG grant Johannes Immergrün a put option to sell the remaining shares.

For its part, Knupp AG would also like to ensure that it can acquire the remaining shares from Johannes Immergrün after the expiry of the five-year lock-up period or that he leaves Immergrün AG as part of the capital reduction. Accordingly, it would also like a call option for the acquisition of the remaining shares of Johannes Immergrün.

1.3.2 Questions

- Does the granting of a combined put and call option qualify as a detrimental breach of the lock-up period within the meaning of Art. 19 para. 2 DBG?

- Does the granting of a put option for the sale of shares in Immer grün AG constitute a breach of the lock-up period?

- How do you assess the granting of a call option to Knupp AG with regard to a possible breach of the blocking period?

- Does the assessment under tax law depend on whether the exercise price for the put or call option is already fixed in terms of amount at the time the option is granted or is merely determined by formula?

1.4 Supplement to the facts 3

1.4.1 Initial situation

Johannes Immergrün's tax advisor is looking for a solution to save the issue tax due on the capital increase in supplement 1. To this end, he proposes the following procedure:

Following the conversion of the sole proprietorship Immergrün into Immergrün AG, which will take place retroactively as at January 1, 2019 for tax purposes, a capital increase will be carried out at Immergrün AG. It is planned to increase the nominal capital from CHF 100,000 to CHF 200,000. The new participation rights are to be issued at nominal value. It is intended that Johannes Immergrün will waive his subscription rights and sell them to Knupp AG at a price of CHF 1,200,000.

1.4.2 Questions

Does the capital increase at Immergrün AG and the associated sale of subscription rights constitute a harmful breach of the lock-up period within the meaning of Art. 19 para. 2 DBG?

Case study 2: The operating requirement as a prerequisite for a tax-neutral conversion

2.1 Basic facts

2.1.1 Initial situation

In addition to their professional activities as asset managers at a major Swiss bank, Fritz Müller and his colleague Peter Scheiff (both 58 years old) also occasionally realize real estate projects as a simple partnership. They acquire plots of land in good locations, have them built on and then sell on the turnkey properties. The gains on the sale were always recorded by the relevant tax authorities as income from self-employment for income tax purposes.

In June 2018, the former simple partnership was entered in the commercial register as the general partnership Immo Müller, Scheiff & Co. Since then, Fritz Müller and Peter Scheiff have each been 50% partners in Immo Müller, Scheiff & Co.

Fritz Müller and Peter Scheiff would like to convert Immo Müller, Scheiff & Co. into a public limited company (Immo MüSchei AG).

2.1.2 Questions

- Does the planned conversion of Immo Müller, Scheiff & Co. into a stock corporation meet the requirements for tax neutrality?

- How are hidden reserves accounted for for tax purposes if the conditions for tax neutrality are not met?

2.2 Supplementary facts 1

2.2.1 Initial situation

In contrast to the basic facts of the case, Fritz Müller and Peter Scheiff have been working as architects for over 15 years and employ a total of 4 people in their architectural practice, which is run as a general partnership.

With regard to the real estate activities of Fritz Müller and Peter Scheiff and the planned conversion into a corporation, reference can be made to the basic facts. In connection with the real estate activities of Fritz Müller and Peter Scheiff, the architecture firm provides various services in the areas of planning, architecture and construction management. These services account for around 20% of the revenue generated by the architectural firm.

Fritz Müller and Peter Scheiff intend to continue their architectural practice unchanged in the form of a general partnership. As part of a long-term succession plan, they are considering involving their longstanding employee Stefan Poller as a partner in the architecture firm. The architecture firm generated a loss in the 2018 financial year, which the previous partners have not yet been able to claim in full.

2.2.2 Questions

- Does the planned conversion of Immo Müller, Scheiff & Co. into a stock corporation meet the requirements for tax neutrality?

- Stefan Poller assumes that, as a new shareholder, he will be able to claim the losses that have not yet been offset on a pro rata basis. Do you agree with his assessment?

2.3 Supplementary facts 2

2.3.1 Initial situation

In the 2018 financial year, the architectural firm of Fritz Müller and Peter Scheiff generated a loss of CHF 400,000 due to extraordinary expenses.

Fritz Müller's wife is also gainfully employed and Mr. and Mrs. Müller were able to offset their share of the loss from the architectural firm in full against other taxable income.

Peter Scheiff is single and did not generate any other income in the 2018 calendar year, meaning that he was not yet able to claim his share of the loss from the architecture firm for tax purposes.

As of January 1, 2019, the architecture firm is now to be converted into a corporation.

2.3.2 Questions

- What impact does the conversion of the architecture firm into a corporation have on the remaining loss carryforward of CHF 200,000?

- The two shareholders agree that Fritz Müller will make an equalization payment of CHF 20,000 to Peter Scheiff because his share of the loss that has not yet been offset can be offset against future profits of the corporation. How is the compensation payment to be assessed for tax purposes?

2.4 Supplement to the facts 3

2.4.1 Initial situation

Based on the initial situation in factual supplement 1, Fritz Müller and Peter Scheiff intend to fundamentally reorganize their professional activities with a view to a later succession plan. They plan to merge the architecture firm and Immo Müller, Scheiff & Co. and then convert the resulting company as a whole into a public limited company.

It is assumed that a real estate project currently being implemented in the canton of Berne will be completed in around 18 months and that the next sale of properties will then take place.

2.4.2 Questions

- Does the tax assessment change if the architectural firm and Immo Müller, Scheiff & Co. are merged and only then converted into a public limited company?

- Does the conversion into a corporation have an impact on the property tax situation of Fritz Müller and Peter Scheiff (all parties and properties involved are in the Canton of Berne)?

- Does the sale of the property after the conversion constitute a breach of the lock-up period or how is the capital gain taxed?

2.5 Supplementary facts 4

2.5.1 Initial situation

As part of a structural reorganization, the architectural firm and Immo Müller, Scheiff & Co. are to merge and continue to operate in the legal form of a general partnership for the time being. However, the two partners decide not to convert the company into a corporation for the time being and to take this decision at a later date.

2.5.2 Question formulation

What are the tax consequences if, at a later date, a Betriebs AG is to be formed with the architectural firm and a Immo-AG with the properties?

Case study 3: Transfer of large real estate assets to a corporation

3.1 Basic facts

3.1.1 Initial situation

A community of co-owners (hereinafter "MEG"), consisting of five heirs each from the "Müller" and "Meier" family lines with four and nine further descendants respectively, owns numerous residential properties (investment properties) in the canton of Berne. The investment costs of the properties total around CHF 30 million and the market value is likely to be around CHF 80 million.

MEG's properties generate annual gross income of around CHF 2.8 million. Administrative management is handled by a contracted property manager, which entails annual costs of around CHF 120,000.

MEG is also the owner of a large plot of building land in the Bern conurbation. On this plot, it is planning - with the assistance of a commissioned architect - a development of 15 terraced houses for its own account with an investment volume (including land value) of around CHF 22 million; the 15 apartments are to be sold as condominiums (of which at least 5 units are to be sold off plan before construction begins). Financing will also be provided by taking out mortgages on the existing (yield-producing) properties.

The properties undisputedly qualify as private assets of the co-owners. In view of the further "fragmentation" of the co-ownership in the coming generations, the parties involved intend to transfer the properties to a stock corporation (hereinafter "MMAG"). Within the framework of the MMAG, it will then tend to be easier to make arrangements (of a statutory and contractual nature) that ensure the MEG's capacity to act and also enable individual participants to leave the company more "easily".

3.1.2 Questions

- What are the tax consequences of transferring the properties to a newly formed company limited by shares?

- Do you see any possibilities of transferring the real estate to the stock corporation with tax deferral?

3.2 Addition to the facts

3.2.1 Initial situation

The MEG is converted into a (commercial) general partnership (Art. 552 CO), whereby all properties, including the aforementioned building land parcel or the corresponding construction project, are transferred into its ownership (Art. 562 CO), with a corresponding entry in the land register of the individual properties. All properties are properly capitalized in the general partnership's accounts (individual valuation in accordance with Art. 960 CO).

3.2.2 Question formulation

Does the conversion of the MEG into a general partnership, combined with the corresponding adjustment of the land register with regard to the individual properties, change the (previous) tax assessment?

Case study 4: Transformation of a corporation into a partnership

4.1 Facts of the case

Mr. and Mrs. Lorenz, who live in Bern, acquired Schönau Gastro AG, based in Thun, in June 2017. They each hold 50% of the shares in the company. The purpose of Schönau Gastro AG is to operate a luxury hotel and a restaurant and it employs around 60 people. The Lorenz spouses are also managing directors of Schönau Gastro AG. They have no other gainful employment. In recent years, the spouses have made considerable investments in the hotel business. In the future, the hotel business is to be further expanded, which will continue to require substantial investment.

In recent years, Schönau Gastro AG has made annual losses in the region of CHF 1.5 - CHF 2.5 million. Schönau Gastro AG's hotel operations only have 28 rooms and are only open during the summer months. A commissioned study has shown that it is very difficult to operate the hotel profitably due to its seasonal nature and the small number of rooms. Accordingly, it can be assumed that the hotel will continue to generate losses in the future (for the time being).

Mr. and Mrs. Lorenz inherited a large fortune from their deceased parents. They invested a large part of the inherited assets in investment properties in various cantons.

The Lorenz spouses have total assets of around CHF 150 million. The investment properties generate annual net rental income of around CHF 3.5 million.

The Lorenz spouses' tax advisor recommends converting Schönau Gastro AG into a general partnership for tax reasons.

Schönau Gastro AG's balance sheet at the end of 2018 was as follows

.png)

Following the transformation of Schönau Gastro AG, Mr. and Mrs. Lorenz will appoint a managing director with many years of international experience in the luxury hotel industry and will no longer perform any operational tasks themselves.

4.2 Questions

- What are the tax consequences of the planned conversion of Schönau Gastro AG into a general partnership? Is the conversion advantageous in terms of a tax-neutral restructuring pursuant to Art. 61 para. 1 let. a DBG?

- What tax and social security consequences may arise if it is expected that the general partnership will continue to generate losses in the future?

Case study 5: Entry of shareholders in partnerships

5.1 Basic facts

5.1.1 Initial situation

Knupp + Co. runs a vegetable growing and trading business in the Bernese Seeland. It is the owner of a warehouse and large tracts of agricultural land. Knupp + Co. is entered in the land register as the landowner. The shareholders are the brothers Kuno and Albert Knupp, each with equal shares.

In view of the succession plan (Kuno is 58 years old and Albert 63 years old), the two partners intend to include Silvan Köhli as a third party in Knupp + Co. The basis for his participation as an equal partner is the company value of CHF 2,100,000 (value as at 2018) as determined by a specialist agency.

The Knupp + Co. trade balance as at December 31, 2018 was as follows (in CHF thousand)

.png)

5.1.2 Questions

- How much money does Silvan Köhli have to "take in hand" to become an equal partner of Knupp + Co.

- How can Silvan Köhli's capital contribution to Knupp + Co. be accounted for (purely accounting options, without tax considerations)?

- What are the income tax consequences, depending on the accounting method?

- Are there any other tax and duty consequences to consider?