Cyrill Habegger

Lukas Habermacher

Pillar 3a

Case studies and detailed solutions from Cyrill Habegger and Lukas Habermacher. This workshop was part of the ISIS seminar "Pensions and Insurance" on September 22 and 23, 2025.

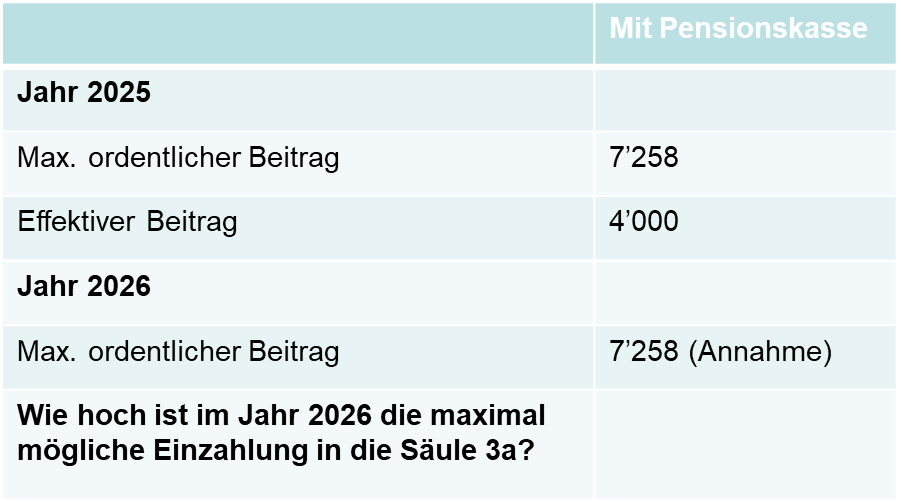

Case 1: Pillar 3a purchase

1.1 Facts of the case

1.2 Question

What is the maximum possible payment into pillar 3a in 2026?

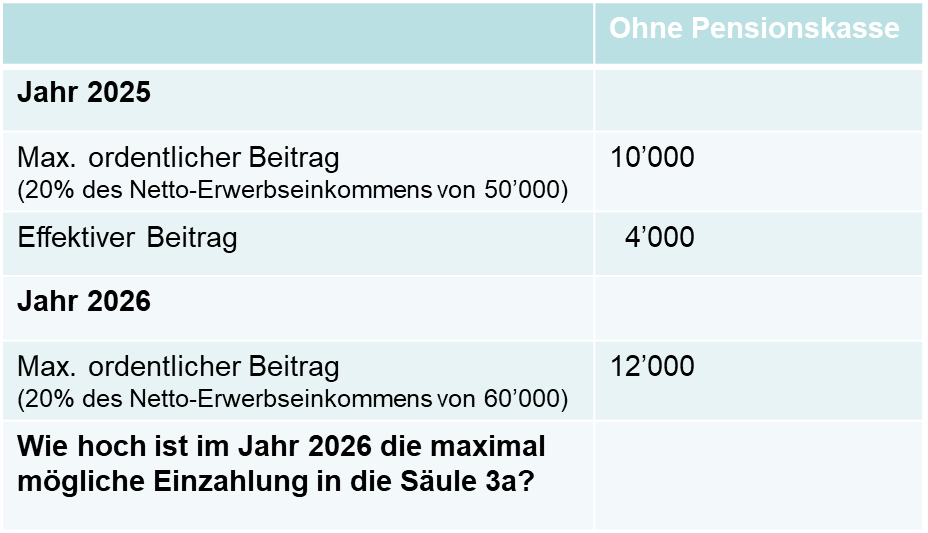

Case 2: Pillar 3a purchase

2.1 The facts of the case

2.2 Question

What is the maximum possible payment into pillar 3a in 2026?

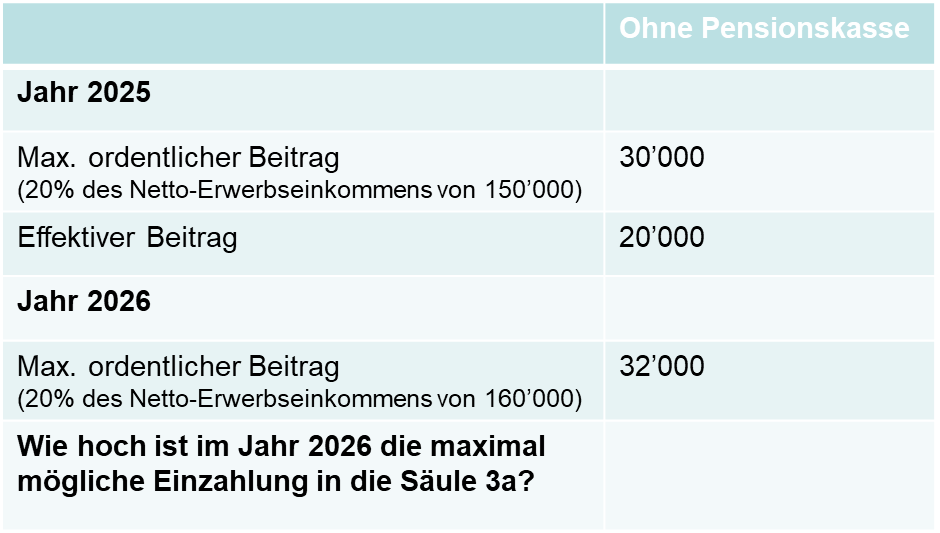

Case 3: Pillar 3a purchase

3.1 Facts of the case

3.2 Question

What is the maximum possible payment into pillar 3a in 2026?

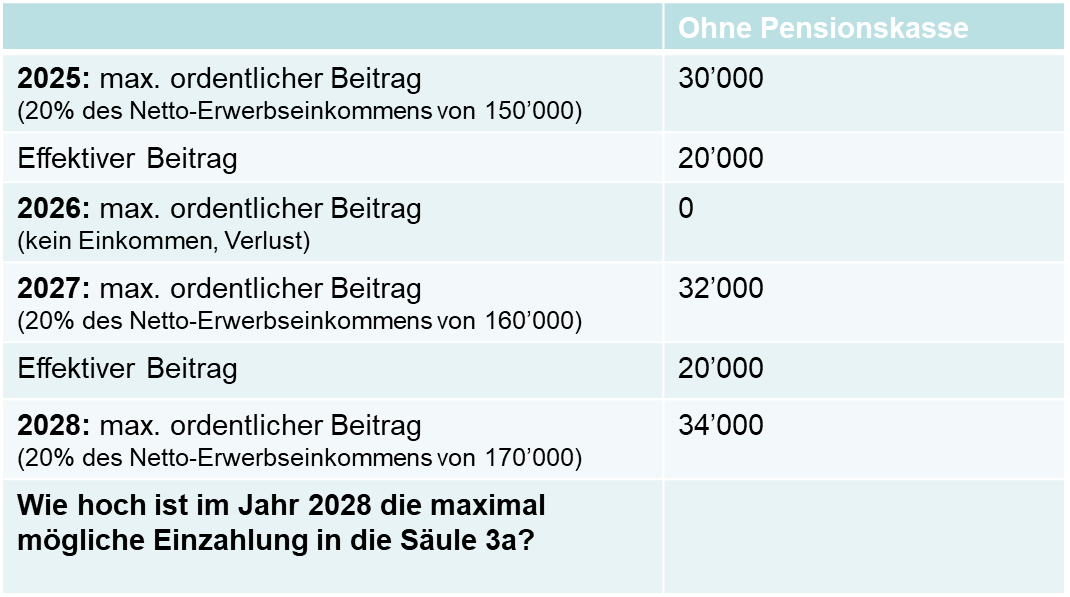

Case 4: Pillar 3a purchase

4.1 Facts of the case

4.2 Question

What is the maximum possible payment into pillar 3a in 2028?

Case 5: Change with PK connection / without PK connection

5.1 Facts of the case

Mr. Müller is gainfully employed until the end of February 2025 and earns CHF 20,000 net. He has his pension fund paid out at the beginning of March 2025 and is then no longer gainfully employed.

5.2 Question

What is the maximum contribution to pillar 3a in 2025?

Case 6: Change with PK connection / without PK connection

6.1 Facts of the case

Mr. Müller is employed until the end of February 2025 and earns CHF 20,000 net. He has his pension fund paid out at the beginning of March 2025, but continues to work until the end of 2025 (income March-December CHF 20,000) without being insured with a pension fund from March 2025.

6.2 Question

What is the maximum contribution to pillar 3a in 2025?

Case 7: Change with PK connection / without PK connection

7.1 Facts of the case

Mr. Müller is employed until the end of June 2025 and earns CHF 45,000 net. From July 2025 to June 2026, he is self-employed and earns CHF 100,000.

7.2 Question

What is the maximum contribution to pillar 3a in 2025?

Case 8: Multiple WEF payments

8.1 Facts of the case

Mr. and Mrs. W. (aged 54 and 55) have a total of four pillar 3a accounts, each with two banks. Each pillar 3a account contains around CHF 150,000.

As the imputed rental value may be abolished and there is a risk of higher taxation of capital benefits from pension plans, Mr. and Mrs. W. decide to amortize mortgages and withdraw the accounts using WEF advance withdrawals as follows:

2025: Ms. W. withdraws her account A from Bank A

2026: Mr. W. draws on his account B at Bank B

2027: Ms. W. draws on her account B at Bank B

2028: Mr. W. withdraws his account A from bank A

8.2 Question

How does this qualify for tax purposes?

Case 9: WEF withdrawal and mortgage increase

9.1 Facts of the case

A (aged 50) withdrew CHF 100,000 from his pillar 3a bank account on 31.10.2024 for the purpose of amortizing an expiring mortgage on his owner-occupied detached house.

In January 2025, A was offered a lower interest rate by his principal bank for the renewal of another fixed-rate mortgage on his single-family home that was due to expire on 31.03.2025 in the event of an increase of CHF 50,000. A accepted this offer.

Option 1: A increases the existing mortgage on his vacation apartment in Ticino by CHF 50,000 as of 01.04.2025.

Option 2: A increases the existing mortgage by CHF 50,000 as of 01.04.2025 to finance upcoming maintenance work on the single-family home.

Option 3: A increases the existing mortgage by CHF 50,000 as of 01.04.2025 in order to finance upcoming maintenance work on the vacation apartment in Ticino.

9.2 Question

What are the tax consequences of the basic situation and the variants?

Case 10: Pillar 3a withdrawal and pension fund purchase

10.1 Facts of the case

A (born 1964) made a purchase of CHF 100,000 into his pension fund on 31.01.2025. The pension fund had previously confirmed to him that his purchase shortfall amounted to CHF 100,000. The purchase was financed from A's freely available savings balance. On 28.02.2025, A closed a pillar 3a account with a balance of CHF 110,000.

10.2 Variant 1:

A closed the pillar 3a account on 31.01.2025. He made the pension fund purchase on 28.02.2025.

10.3 Variant 2:

On 31.01.2025, A requested the direct transfer of CHF 100,000 from his pillar 3a account (balance: CHF 110,000) to his pension fund in order to finance the purchase.

10.4 Question

What are the tax consequences in the basic case and in the two variants?

Case 11: Genuine and non-genuine ANOBAG

11.1 Facts of the case

X., a Swiss national, works for a Chinese (alternative 1: German) industrial company as a sales manager for Europe. X. is resident in Switzerland and receives a fixed salary as a self-employed person. Because the Chinese (German) company does not have a permanent establishment in Switzerland, it does not pay AHV contributions (Art. 12 AHVG). X. pays his AHV contributions himself in accordance with Art. 6 AHVG (so-called 'ANOBAG') or via an agreement in accordance with Art. 21 VO 987/2009.

11.2 Question

Can X. accumulate a pillar 3a? If so, to what extent?